Samsung Speeds Up Effort to Shutter Large-Size LCD Production Lines

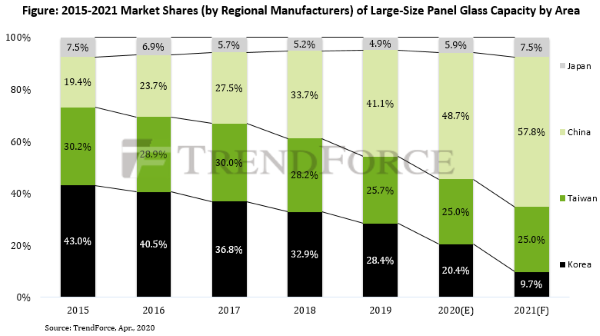

As Samsung Display Co. (SDC) buckles under the pressure of oversupply and pandemic-induced operating difficulties, the company has made the decision to exit the LCD panel manufacturing business. According to the latest investigations by the WitsView research division of TrendForce, the rapid decline of Korean manufacturers’ large-size panel glass capacity by area in 2020 is projected to result in a drop in market share from 28.4% in 2019 to 20.4% this year. The production capacity of Chinese panel manufacturers is expected to continue expanding in 2021. This growth, combined with the capacity shortfall from SDC’s discontinued LCD manufacturing, is expected to lead to Korean panel manufacturers’ large-size panel capacity by area to drop below 10% market share.

TrendForce Senior Research Manager Anita Wang indicates that SDC planned to terminate all of its LCD production lines, including the Suzhou fab, by 4Q20. Similarly, LGD intended to close down its Gen 7.5 production lines in 4Q20, in turn resulting in a 19.7% decrease YoY in total Gen 7.5 glass capacity by area in 2020 and a 42.2% decrease in 2021, with only two suppliers, AUO and Innolux, remaining as the sole Gen 7.5 glass suppliers. TV panels supplied by SDC’s Gen 7.5 fabs are primarily 75-inch and 82-inch panels. Therefore, clients have preemptively shifted their demand for 82-inch panels to 85-inch panels, since the latter has a healthier supply level; orders for 85-inch panels are fulfilled by AUO and CSOT. On the other hand, LGD’s Gen 7.5 fabs primarily manufacture 43-inch IPS TV panels. Following the closure of LGD’s Gen 7.5 fabs, orders for 43-inch IPS TV panels will be fulfilled at BOE and HKC’s Mianyang fabs.

SDC’s closure of its Gen 8.5 LCD fabs is projected to lead to a 3.2% decrease YoY in total Gen 8.x production capacity by area in 2020. This figure is likely to further expand to a 6.3% decrease in 2021. In any case, the magnitude of these reductions is still relatively minor compared to reductions in Gen 7.5 production capacity, since newly added capacity from HKC is expected to shore up the decline in Gen 8.x capacities.

Despite the newly added large-size panel glass capacities by non-Korean panel manufacturers, the massive capacity reduction of Korean manufacturers means total panel glass capacity by area in 2020 and 2021 will not see a continuation of the 2018/2019 growth surge, with 2020 keeping flat with 2019 figures, and 2021 undergoing a 0.9% decrease YoY.

Microsoft Teams

Microsoft Teams WhatsApp

WhatsApp Email

Email Inquiry

Inquiry WeChat

WeChat

TOP

TOP